Introduction

Cross-chain MEV refers to the potential profit that can be earned by miners or validators by exploiting information asymmetries across different chains. For example, suppose a price discrepancy exists between a cryptocurrency on one blockchain and the same cryptocurrency on another. In that case, a miner or validator could potentially buy the cryptocurrency on the cheaper blockchain, transfer it to the more expensive blockchain, and sell it for a profit. By doing this, the miner or validator is exploiting the price discrepancy and earning cross-chain MEV.

This report summarizes the findings of our analysis of the cross-chain MEV arbitrage opportunity of $ATOM across 4 different chains (Osmosis, Cronos, Canto, and Evmos). The source code used to produce this analysis are available for for exploration on our github. Take a look, hack at it, otherwise let’s dive into the our analysis.

Approach

- We took the pools with the highest amount of ATOM liquidity and the corresponding token pair in each of the 4 chains (Osmosis, Cronos, Canto, and Evmos)

- We used the following Dexes and their corresponding pairs and a rough estimation of their liquidity ranges during the analyzed period:

- We looked at data between October 28th, 2022 and January 25th, 2023

- We calculate the cross-chain arbitrage opportunity size as the absolute sum of price differences across chains.

- There is either low or non-existent IBC volume between Canto, Evmos, and Cronos plus tokens might still need to be routed through Osmosis to avoid different denomination paths. Hence we decided to look only into the price differences between these three chains against Osmosis.

- Raw data is at the second (time) level but we grouped each 1-second entry into 6-second groups and averaged their price to simulate Osmosis blocks to market-size the opportunities more realistically. This is important because an opportunity of $1 over 12 seconds would yield $12 whereas an opportunity of $1 for two blocks is only $2.

- To measure price discrepancies, we use thresholds that we call price difference tolerance. A price difference tolerance of 1% would suggest that the price difference is higher than 1%. For example, an asset with a price of $100 in Osmosis and $102 in another chain would have a price difference of 2% and would consequently fall under this classification.

- Limitation: when calculating opportunity size we lacked token ratio and liquidity numbers with the same resolution of the price data. We do take the liquidity differences into account and we explain below what this means for the results.

- The data sets and code can be find in our research public repo: https://github.com/meka-dev/research/tree/main/Reports/Cross-chain Arbitrage Analysis

How big is the cross-chain arbitrage opportunity?

Our goal with this report is to descriptively give a picture of initial cross-chain MEV numbers to spark debate and help cosmonauts understand this new ecosystem.

For the scope of this analysis, we only looked at the theoretical arbitrage opportunity. By theoretical we mean the absolute amount of USD available in price differences across chains, which at the end of the day is the maximal amount that a trader could in theory capitalize on. In practice, things are different because we need to take slippage into account. This means that the actual amount of opportunity is less since slippage would end up decreasing the output amounts of the trades. We lack the data to assess the exact token rations and liquidity amounts at each block but are working with partners to get our hands on them.

As we can see here, the differences in $ATOM prices in Evmos and Osmosis present the most profitable opportunities, however, we also know that Evmos had the lowest liquidity of all the pools, so the actual opportunity would certainly decrease the most for Evmos compared to Cronos and Canto. We hope that this analysis gives cosmonauts not just ammunition for discussion but also an initial framework on how to start looking into cross-chain MEV.

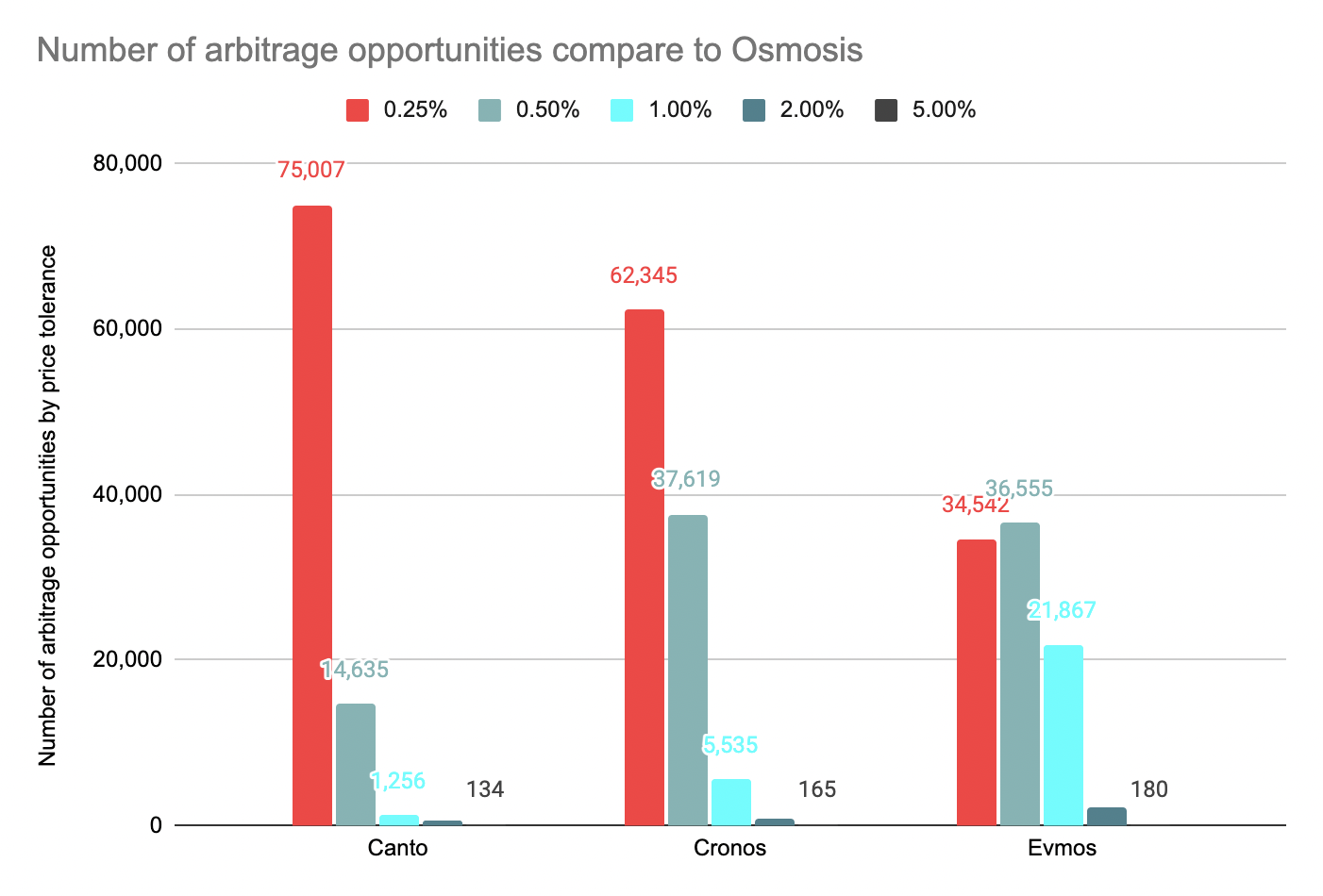

How many opportunities are there?

As expected, high-price discrepancies happen very rarely. For example opportunities above 5% in price difference average about 1.5-2 per day depending on the chain. Additionally, we saw Evmos having the highest amount of opportunities higher than 0.5% against Osmosis. Evmos is also the chain with the lowest amount of liquidity, so it’s something we would also expect. A swap in a low-liquidity pool with substantial volume would have higher slippage and hence generate a higher price difference in comparison with other chains.

Average time with price discrepancies

In order to have a clearer idea of how often these opportunities arise we looked into the percentage of time in which there are price differences across these chains based on the corresponding price tolerance.

Here we can see that Evmos also has the highest amount of time of open opportunities against Osmosis up to a price difference of 1%.

There are two important observations:

- Even though the theoretical opportunity against Evmos is higher given the higher amount of time these differences are created. 19.94% of the time there is a price discrepancy of at least 1% between Evmos and Osmosis. This indicates that the opportunity is not being capitalized as fast as the other chains. The likely thesis is that the lower liquidity on Evmos either obliges traders to ignore the less profitable opportunity given the potential slippage or is not being capitalized at all.

- Price differences of at least 0.5% happen only 5.30% of the time between Osmosis and Canto vs 25.89% and 56.73% in Osmosis-Cronos and Osmosis-Evmos respectively. Canto is indeed the highest liquidity chain from the other Comparison chains, which suggests again that high-liquidity pools will present the lowest time of open opportunities.

Visualizing the differences

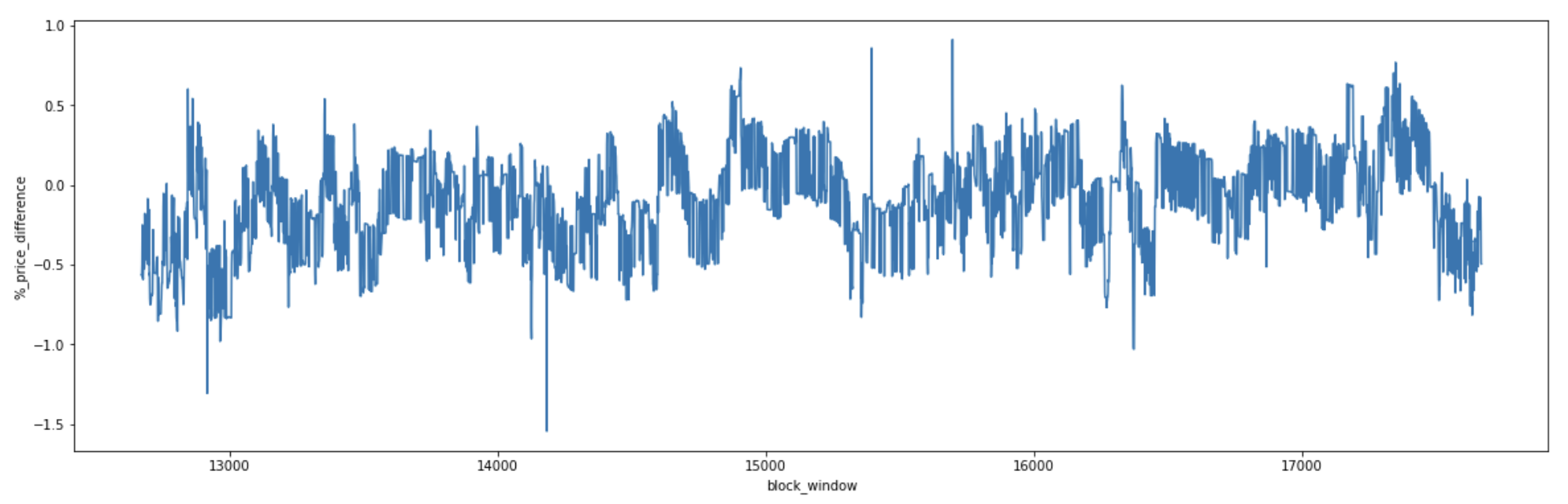

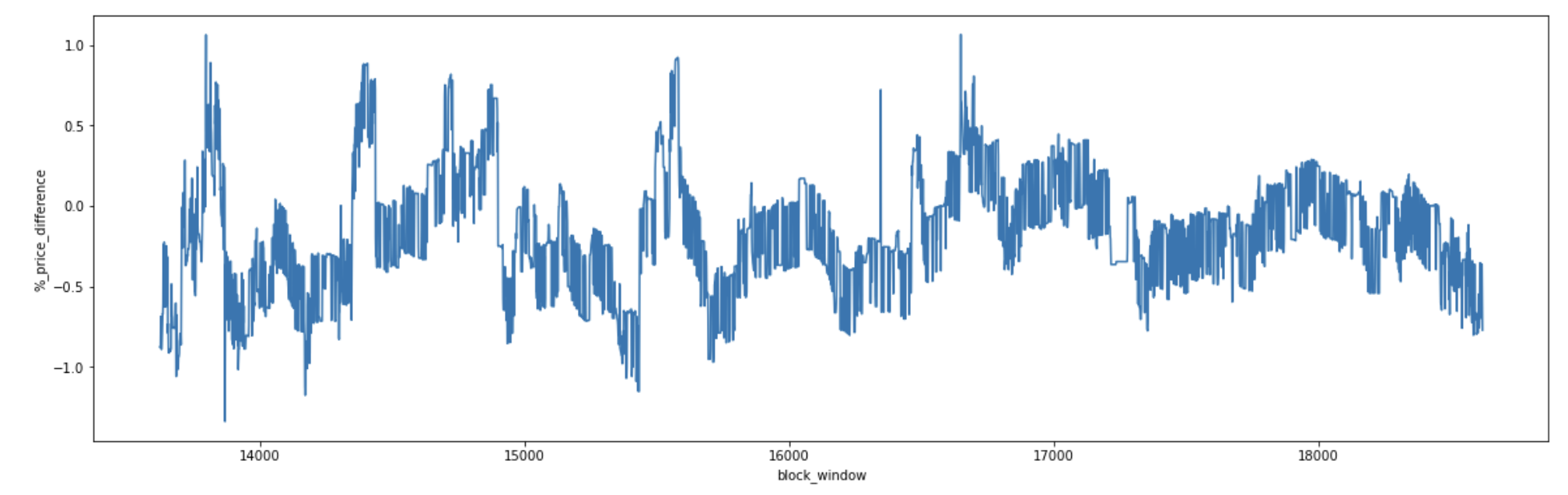

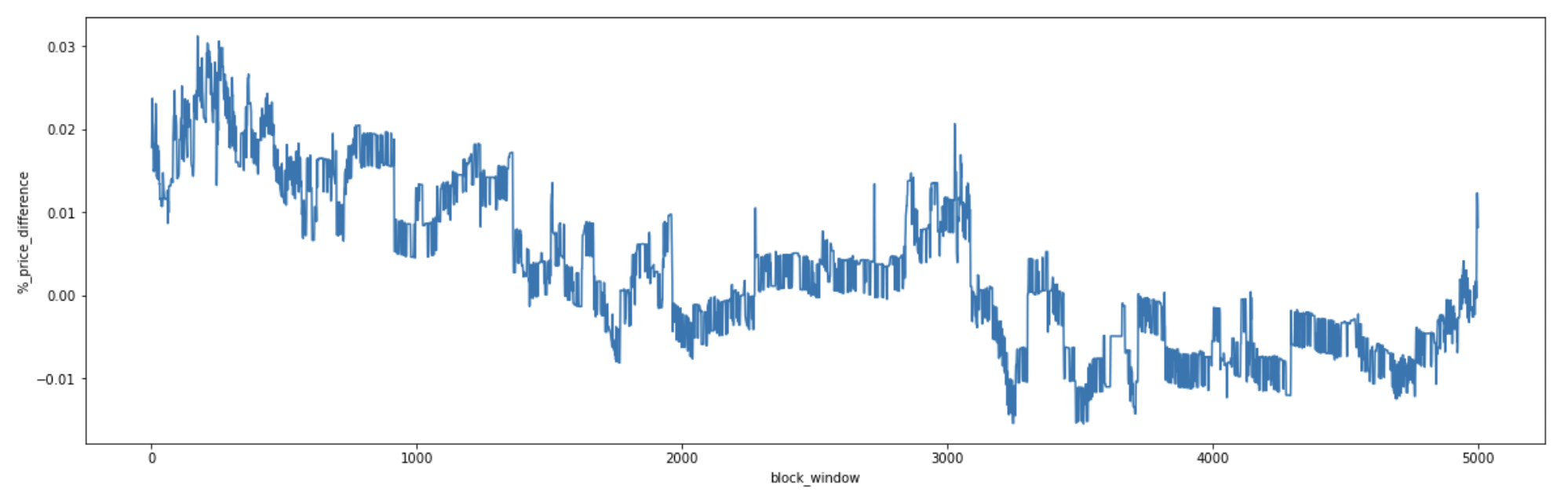

In order to make it easier to understand how these differences manifest over time we’ve taken a small slice of the first initial pairs in the table above to demonstrate how these variances look in the data. We’ve decreased the resolution to 6-second blocks (block_windows) to replicate the Osmosis blocks.

Osmosis-Canto

0.83% of the time >1% price difference

Osmosis-Cronos

4.33% of the time >1% price difference

Osmosis-Evmos

20% of the time >1% price difference

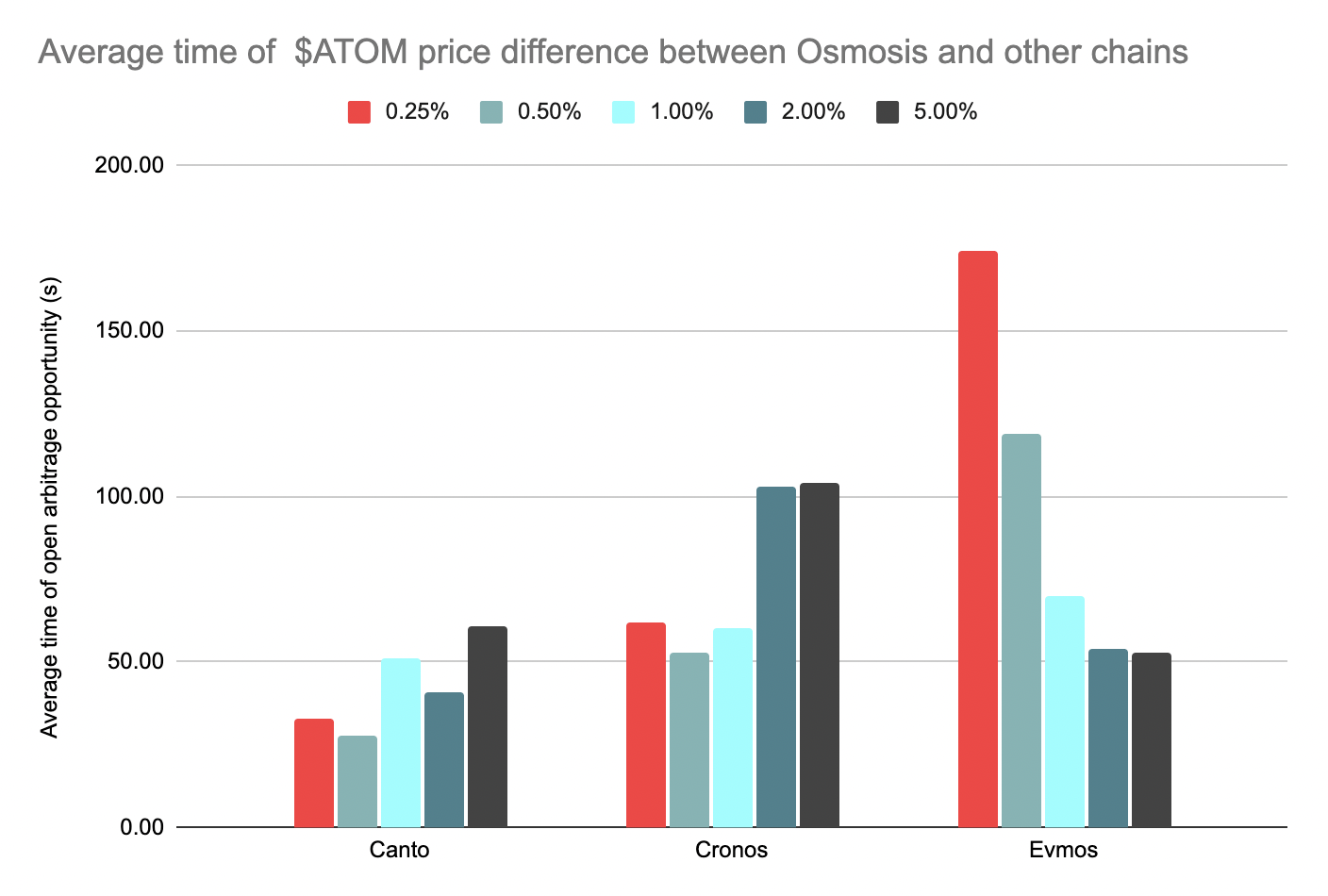

How long does it take for an opportunity to close?

We looked at specific instances where there were increases in price differences and calculated how long it took for the opportunity to close again.

The average time of opportunities across Osmosis and Canto, which are the two chains with the highest liquidity, have lower variance. However, 5%-tolerance opportunities take the longest to close. This correlation can also be seen in Cronos, where the highest price discrepancies also take longer to close. On the other hand, we see the opposite in Evmos, where low price discrepancies take longer to close and high price discrepancies close relatively quickly.

A possible explanation is that opportunities between Osmosis-Canto and Osmosis-Cronos are not been taken advantage of. Looking at IBC volume, according to MapOfZones in the last 30 days as of the date of this article, Evmos has 3 times as much IBC volume with Osmosis as OsmosisCronos and 100 times more than Osmosis-Canto, which could be an indication of this thesis. On the other hand, Osmosis-Evmos data indicates that high-price opportunities are been capitalized on and low-price ones are been ignored.

Conclusion

In this article, we were able to give the Cosmos ecosystem the first numbers into cross-chain MEV, more specifically the arbitrage opportunities of $ATOM across different Cosmos chains. We were able to calculate the theoretical opportunity size, with the limitation that we lacked data about the pool depth to give a more precise picture. The current analysis suggests that there is fairly little profit being made and potential opportunities seem to even be ignored across some of these chains. Additionally, we were able to calculate how long these opportunities exist and hope this paves the way for arbitrageurs and other MEV players to start developing a cross-chain MEV strategy that we believe is crucial for the sustainability of all Cosmos chains.